Curve describes itself as the Netflix of banking. Of course – these days, every new app is the ‘insert-industry-here’ version of Netflix. Is this comparison justified, and if it is, do we really need a Netflix-style carousel for our bank accounts? A customer review on the Curve website seems to think so, describing it as ‘one of those inventions that once you use it, you wonder why the hell you didn’t have it sooner’.

The collation of bank accounts into one quick, easy access point is a seemingly obvious opportunity, and yet, no one managed it until Curve came along. In this article, we’re discussing what it is exactly, how it works, and if it’s worth your time.

What is Curve?

Curve is not a bank, but a ‘meeting point’ for your existing banks. You can enter on one of 3 levels: Curve Blue, the free version, Curve Black, which costs £9.99 per month, and Curve Metal, the £14.99 per month premium version. You can link all Mastercard and Visa accounts (but not Amex at the time of writing).

What are the perks of Curve?

The USP of Curve is that it allows the user to pay with any credit and debit card, at any given time, without having to carry any of them around. But there are a few extra perks to sweeten the deal…

No fees abroad

Fee-free foreign spending comes as standard, with all of the free and paid tiers. There are limits:

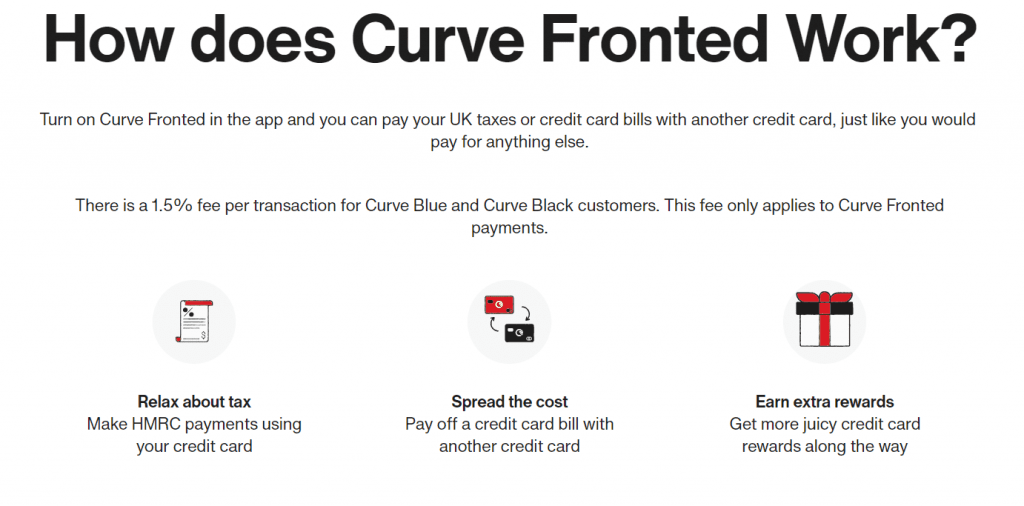

Curve ‘fronted’

This is a pretty special feature which allows you to pay for things that wouldn’t usually accept credit, like HMRC bills and other credit card bills. You’ll pay a 1.5% fee on Curve Blue and Black, but it’s free on Curve Metal.

Collated spending analysis

Online banking apps have enabled users to view their spending habits on easy-to-interpret pie charts for a while now, but Curve is the only app that allows you to view all your cross-account spending in one place. Much easier than analysing each of them separately.

Go back in time

Perhaps one of the most interesting features about the Curve system is the Go Back In Time feature. It allows you to change your mind about which account you used to pay for something, for up to 90 days after the fact. If you made a large purchase on your debit card, but want to free up some cash, you can reroute the payment back through your credit card.

Cashback

Curve Blue (the free version) earns you 1% cashback from 3 retailers of your choice for 90 days. With Black, you get the same, but with no time limit. Metal also returns 1%, but with 6 retailers of your choice, and again with no 90 day limit. It’s a nice bonus, but some credit cards earn higher returns, so make sure you weigh it up against other options if cashback is your priority.

Are there any downsides to Curve?

ATM limits

The three Curve tiers impose £200, £400 and £600 monthly ATM withdrawal limits respectively. If you regularly use cash for large purchases, this may be something of an annoyance.

Section 75 protection

Section 75 is a protective measure afforded to all credit card purchases between £100 and £30,000. It means your credit card provider and the retailer are jointly responsible for ensuring you get your money back if things go wrong. Curve doesn’t fall under this protection, but it does cover you under the Curve Customer Protection, which is similar.

Common sense

There’s also the convenience trap aspect of putting everything in one place. If you get used to carrying just one card, and you lose it, you might find yourself left without backup. It’s always a good idea to carry a spare card somewhere other than your wallet in case the worst happens.

Weekend FX Fee

If you make a withdrawal or purchase over the weekend and Curve performs a currency conversion, they will use the rate from the last working day and apply a surcharge as the Forex markets are closed. The weekend counts as Friday 23:59 GMT – Sunday 23:59 GMT including any bank holiday. For transactions where both the transaction and the underlying payment cards are in the following currencies; GBP, USD or EUR, the foreign exchange fee will be 0.5%. For all other currencies, the foreign exchange fee will be 1.5% more information can be found here.

Curve Card Options

Free | £9.99/month | £14.99/month | |

| Combine Your Cards | Yes | Yes | Yes |

| Google Pay, Samsung Pay & Apple Pay | Yes | Yes | Yes |

| iOS & Android App | Yes | Yes | Yes |

| Curve Customer Protection up to 100,000€ | Yes | Yes | Yes |

| Go Back in Time: Move 90-day old payments, up to 5,000€ | Yes | Yes | Yes |

| Access to fair FX rates (additional fees may apply) | Access up to 500€/month | Unlimited access | Unlimited access |

| Fee-free foreign ATM withdrawals (weekend charges apply) | 200€/month | 400€/month | 600€/month |

| Curve Cash: 1% Cashback | 3 selected retailers (unlimited time) | 6 selected retailers (unlimited time) | |

| Worldwide Travel Insurance | Yes | Yes | |

| Mobile Phone Insurance | Yes | ||

| Worldwide Airport LoungeKey Access | Yes | ||

| Rental Car Collision Waiver Insurance | Yes | ||

| Premium 18g metal card (3 colours) | Yes |

Is Curve Metal worth the cost?

Curve Metal sounds expensive at £14.99 per month, but when you look into the perks, you’ll understand the pricing. This is where the Curve lifestyle really ramps up a gear, with travel insurance, phone insurance, rental car insurance, and – our favourite – discounted access to airport lounges worldwide.

If you’re already paying £10-ish a month for phone insurance and you’re considering Curve, going for Metal is a no brainer. The daily spending limit increases from £2,000 to £3,750 per day with Curve Black and Metal. There’s also the fact Curve Metal literally is made of metal, and three times heavier than your average credit card… if that floats your boat.

Is Curve right for me?

The answer to this is a simple one, and it comes down to how many cards you regularly carry. If your banking is centered around a current account and a credit card, or you use Apple Pay for everything, it’s probably not worth your while. But if you find yourself regularly switching between three or more separate accounts – for example debit, credit, and business accounts – you may find Curve makes it much easier not only to pay instantaneously and without carrying around multiple cards, but to keep track of your spending.

The point of Curve isn’t just convenience, but intelligent tracking and managing. It’s currently the only way to view all of your cross-bank transactions in one place, so if you’re hot on budgeting, it’ll save you manually pulling together all of your accounts into one spreadsheet.

If it’s the perks you’re after, like no foreign spending fees and instant notifications, you can find these with other mobile banking apps like Monzo and Starling. But the Curve Metal insurance benefits really add another string to its bow, and the ability to add non-UK cards is a huge bonus for the more itinerant spenders.

{kind=link}